Guide to Roth conversions for surviving spouse and heirs

Whenever I have an initial conversation with a potential new client, I mention how taxes and investing are “joined at the hip.” You don’t want to let the “tax tail wag the dog” (meaning you don’t want...

Whenever I have an initial conversation with a potential new client, I mention how taxes and investing are “joined at the hip.” You don’t want to let the “tax tail wag the dog” (meaning you don’t want to let taxes drive decisions), but you also don’t want to ignore taxes. In this blog, I’ll show how Roth IRAs (and Roth conversions) can lower lifetime taxes for you—including Roth conversions for surviving spouse scenarios—your heirs, and when they may not.

I’ve written about Roth conversions several times before (see Roth Conversion Benefits Can Apply More Broadly, Roth Conversions and Low Rates, Roth Conversions and New Beginnings, and 7 Benefits of a Roth IRA). Roth conversions are an important consideration in any financial plan. If you want to read more about Roth IRAs, this article discusses some of the pros and cons of Roth IRAs. Read this one if you want to learn more about how to do a Roth conversion.

Roth Conversion Quick-Check (This Year)

· My estimated taxable income and deductions are updated.

· I know my comfortable top bracket (e.g., 22%/24%).

· I checked IRMAA thresholds (two-year lookback).

· I’m not jeopardizing ACA premium credits (if <65).

· Conversions work best when you pay the tax from taxable cash on hand.

· I’m okay with the five-year conversion rule.

Traditional IRAs vs. Roth IRAs

Traditional (tax-deferred): Traditional Individual Retirement Accounts (IRAs) and workplace plans (401(k)s, 403(b)s). You may receive a deduction for contributions, growth is tax-deferred, and withdrawals are taxed as ordinary income.

Roth (tax-free later): Roth IRAs and Roth options in workplace plans. You pay tax now, growth is tax-free, and qualified withdrawals are tax-free later.

Initial Funding of Roth IRAs

Unless you’re someone like Peter Thiel, it’s hard to build a large balance in a Roth IRA only through contributions. You can contribute up to $7,000 per year ($8,000 if you are 50 or older). Income limitations also apply. By 2026, most (if not all) employers will likely offer a Roth option in their 401(k) or 403(b) plans. If yours does, you can contribute up to $23,500 this year ($31,000 for those 50 or over). Under a rule change in SECURE Act 2.0, employees aged 60, 61, 62, and 63 can make a higher catch-up contribution of $11,250 in 2025 rather than $7,500. The catch-up amount represents the higher of $10,000 indexed for inflation, or 150% of the regular catch-up amount. Beginning in 2026, highly compensated employees will be required to make all catch-ups as Roth contributions in workplace plans.

Those with income exceeding the contribution limit could complete backdoor Roth conversions to get around the income limits for IRA contributions. (In short, a backdoor Roth involves making a nondeductible IRA contribution and then converting it to a Roth IRA.) Generally, you should attempt a backdoor Roth IRA only if you do not have any funds in traditional IRAs or rollover IRAs. Having such accounts can make your backdoor Roth IRA conversion taxable. Backdoor Roth conversions trigger the pro-rata rule across all your IRAs and require the completion of IRS Form 8606. If you hold any pre-tax IRA money, get advice before proceeding.

If your plan allows after-tax contributions and either in-plan Roth conversion or in-service rollovers, a “mega backdoor Roth” can move substantially more into Roth than the employee deferral limits alone.

Another way to fund your Roth IRA is by converting funds from your traditional IRA to a Roth IRA. For a Roth conversion, you pay tax on any untaxed amounts that you convert.

Why Roth Dollars Matter

There are many types of diversification. Most people have at least heard of the term asset allocation. This approach involves holding assets across multiple asset classes to diversify your investments and mitigate risk. It’s also important to consider asset location—placing certain assets in certain accounts for better tax efficiency (e.g., higher-growth equities in a Roth).

SECURE Act 2.0 note: No RMDs from Roth 401(k)/403(b) beginning in 2024.

You also want to diversify your account types. By this, I mean you should try to have accounts that are treated differently from a tax perspective. This can allow you to better manage your tax bill. Withdrawals from taxable accounts, IRAs, and Roth IRAs are all taxed differently. By considering your tax situation in any given year, you can make your withdrawals more tax-efficient. How? You can balance the amount you withdraw from each different type of account. That can help you minimize your tax bill. The potential benefits of Roth IRAs include a lower tax bill over time

Please note that this blog does not address Health Savings Accounts (HSAs). When paired with a high-deductible health plan, HSAs can be even more tax-efficient than IRAs or Roth IRAs: contributions can be tax-deductible, growth is tax-deferred, and withdrawals for qualified medical expenses are tax-free. Notably, medical expenses for this purpose generally include qualified expenses incurred any time after the plan was established.

Tax Benefits of Roth IRAs

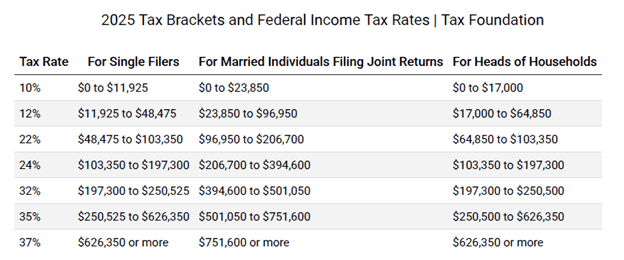

Roth conversions can help you increase the amount you hold in a Roth IRA. They can also help you better manage your tax bill. Let’s talk about how. The following table shows the 2025 tax brackets for different filing statuses.

Sources: Internal Revenue Service, “Revenue Procedure 2024-40” and Tax Foundation.

In a historical context, a tax rate of as much as 24% remains low. When it comes to paying taxes, I like to discuss the idea of bracket-filling. What I mean by that is, based on your current income and assets, determine the maximum tax rate you’re willing to pay. I find that clients are usually willing to pay taxes at a rate of 22% or even 24%. (For some, it’s only 12%.) It all depends on your situation.

Bracket filling in 3 steps:

Estimate your taxable income for the year.

Pick the top bracket you’re comfortable paying (e.g., 22% or 24%).

Convert just enough traditional IRA dollars to “fill” the remaining room in that bracket—without spilling into the next one.

I want to compare the rate you will pay today to the rate you might pay in the future. Please note that I do not, in any way, pretend I have a crystal ball that allows me to predict future tax rates with any degree of certainty. I prefer to default to whatever I currently know about tax rates. If rates change in the future, I will change my views to reflect those changes.

Benefits of Roth IRAs for Married Couples

For purposes of this discussion, I’m going to focus on Married Individuals Filing Joint Returns. Consider a married couple that expects to earn $300,000 of taxable income in 2025. Their marginal tax rate – the tax rate paid on the last dollar of income – will be 24%.

Let’s also assume that this couple regularly contributes the maximum amount to their IRAs. Based on their financial plan, we project they will have $3.0 million in their IRAs upon retirement. (Please note: I understand these numbers may seem high. But they are more achievable than you think if you can earn a good income and save diligently toward retirement.)

Now, let’s project that when they retire, they will receive combined annual Social Security benefits of $80,000. A few years into retirement, their required minimum distributions (RMDs) could be as high as $150,000 or more. (For context, at age 80, the IRS factor is 20.2, so a $3 million IRA implies an RMD of $148,515. If your IRA balance continues to increase or remains relatively the same, future RMDs may be even larger.) Let’s also assume they have $30,000 of other income. That could put them into the 32% tax bracket. That’s 8% higher than what they pay today. Even if it doesn’t, the following sections explain why a Roth conversion could still save taxes over the long term.

Roth Conversions for Surviving Spouse: Why Filing Status Matters

More often than not, one spouse outlives the other. Sorry, guys, but usually our wives outlive us. What happens now from a tax perspective highlights another benefit of having your money in a Roth. After the first spouse dies, the survivor often files Married Filing Jointly (MFJ) for the year of death and Single thereafter. Roth conversions for surviving spouse can reduce lifetime taxes by shifting pre-tax IRA dollars into Roth IRAs while you’re still filing jointly. After death, similar withdrawals hit higher Single brackets and may raise IRMAA. Planned conversions at 22%–24% today can beat 32%–35% later.

IRMAA brackets can also change with filing status. As a planning checkpoint, model Roth conversions for surviving spouse across two filing statuses (MFJ this year, Single next year) and compare IRMAA impacts.

Most of the income you receive in retirement as a couple will go to your wife after you die. Your wife gets the higher of the two Social Security benefits. We usually pass our IRAs to our spouses first. That means her RMD won’t change significantly from what you take as a couple. If she’s younger, her RMD may be slightly lower.

Assume that your Social Security benefits were about the same. That leaves her with $40,000 of Social Security income. If the account grows and/or at older ages, RMDs can reach $ 300,000 or more; that’s where earlier conversions can matter most. Let’s look at what can happen. We calculate an RMD of $300,000. Other income remains at $25,000, and Social Security benefits are $40,000. That translates to $365,000 of income. If we use the 2025 tax table, as a single filer, she’ll be in the 35% tax bracket. In this case, paying tax on a Roth conversion at a 24% rate today clearly results in long-term tax savings.

Benefits of Roth IRAs to Your Heirs

Some of us want to leave money to our children after we pass away. Some don’t. Others say if some money is left after they’ve passed, it will be nice, but it’s not a priority.

With the passage of the SECURE Act on December 27, 2019, the rules for inherited IRAs changed. Non-spouse heirs generally must empty inherited IRAs within 10 years. This can create what I like to refer to as a “tax bomb” (or a large unexpected tax bill) for your beneficiary. The additional income can put him or her—or their family—in a higher tax bracket.

Inherited Roth IRAs can be left to grow for up to ten years and then withdrawn tax-free.

If your beneficiary inherits money held in a Roth IRA, they still have only 10 years to distribute it, but they won’t pay any taxes on it. They can also let the cash sit in the Roth IRA for the full 10 years, where it can continue to grow tax-free.

Don’t Forget the Roth Conversion 5-year Rule

When you make Roth conversions, you also want to keep the “Roth conversion 5-year rule” in mind. You must consider two separate rules: the general five-year rule for the Roth account itself, and the conversion-specific five-year rule.

Roth contributions: earnings are tax-free if 5 years have passed and you’re 59½ (or meet another qualified event).

Roth conversions: each conversion has its own 5-year clock; withdrawing converted amounts within five years and before 59½ can trigger a 10% penalty.

Other Roth IRA Considerations (Social Security and Medicare-Related Concerns)

There are a few additional considerations to keep in mind regarding Roth conversions. They can have positive or negative effects on your taxable income and tax bill in other ways. You need to be aware of the potential negative consequences that higher taxable income resulting from Roth conversions can have on your tax bill. On the other hand, Roth conversions can benefit your tax bill by reducing future income.

For example, consider the Social Security tax torpedo. As provisional income rises, up to 85% of Social Security benefits become taxable. This can result when your income crosses certain thresholds. Higher income can make more of your Social Security benefits taxable. You also want to consider the impact that higher income can have on your Medicare premiums. Your monthly premiums can increase when your income rises. This increase is referred to as IRMAA, the Income-Related Monthly Adjustment Amount. IRMAA uses a two-year lookback on MAGI (so 2025 conversions affect 2027 premiums).

While Roth conversions increase (modified adjusted gross income (MAGI) now, due to the two-year lookback and filing status changes, they can lower MAGI later. As a result, future IRMAA and the share of Social Security subject to tax (up to 85%) can be lower.

FAQs: Why Roth IRAs Matter (and How to Use Them Wisely)

1) Why do you say taxes and investing are “joined at the hip”?

Because every investment move has a tax consequence. We don’t let the tax tail wag the dog, but we also don’t ignore taxes. Smart tax choices can lower today’s bill and leave you more to spend later.

2) Roth vs. traditional: what’s the real difference?

Traditional (IRA/401k/403b): Pre-tax contributions, tax-deferred growth, taxed when withdrawn at ordinary income rates.

Roth (Roth IRA/401k/403b): After-tax in, tax-free growth, tax-free withdrawals (if rules met).

Both are tax-deferred while invested; the difference is when you pay tax.

3) How can I get money into a Roth?

Direct contributions: Typically, up to the annual limit (with income limits for Roth IRAs).

Work plans: Many 401(k)/403(b) plans offer a Roth option with higher deferral limits.

Backdoor Roth IRA: Make a non-deductible IRA contribution, then convert—best if you don’t have other pre-tax IRA balances (pro-rata rule). Congress has floated curbing this in the past; treat it as available until it’s not.

Roth conversion: Move pre-tax IRA/401(k) dollars to Roth and pay tax now.

4) When do Roth conversions make the most sense?

In lower-income years (often post-retirement, pre-RMD).

When you can “bracket-stuff” at a rate you’re comfortable with (e.g., 22%–24%).

5) Who benefits besides me—my spouse and my heirs?

Spouse: After the first death, the survivor’s filing status usually shifts to Single while RMDs and income often remain high—pushing the survivor into higher brackets. More Roth dollars mean fewer taxable RMDs.

Heirs: Under the SECURE Act, most non-spouse heirs must empty inherited accounts within 10 years. Inheriting Roth avoids a taxable “tax bomb.”

6) What about Medicare IRMAA and the Social Security “tax torpedo”?

Conversions raise modified adjusted gross income (MAGI) in the year you convert (can trigger IRMAA two years later and pull more Social Security benefits into taxable income). Done thoughtfully, conversions lower future MAGI, helping reduce IRMAA and mitigate the torpedo later. This is why we size conversions annually, not one-and-done.

7) How do Roths fit into my bigger plan (asset location & tax diversification)?

Aim for tax diversification across taxable/pre-tax / Roth buckets. That lets you blend withdrawals each year to reduce your lifetime tax bill. Pair that with asset location (what goes where) to boost after-tax results.

If you’d like help sizing a Roth conversion (often a Q4 exercise once income is clearer), I’m happy to run the numbers and map a year-by-year plan.

Bottom Line

Many of us have low balances in our Roth IRA accounts – perhaps you don’t have any Roth IRAs at all. The contribution limits are low. They haven’t been around that long either – they were not a savings option until 1998. That doesn’t mean that Roth IRAs should be disregarded. They can still play an essential role in your financial plan. The potential benefits of Roth IRAs, as discussed above, are a key consideration when working on your financial plan.

If you don’t have a Roth IRA – or only have a small amount in your Roth IRA – you can still consider Roth conversions. Roth conversions can add value to us in three different phases of our lives:

They can lower the cost of withdrawing funds from our retirement accounts.

They can reduce the taxes paid by a surviving spouse.

The tax bill for our beneficiaries in future generations can also be lowered.

While you can have an overall intention to complete Roth conversions as part of your financial plan, you should decide how to proceed on a year-by-year basis. When I work with clients on this type of issue, in the fourth quarter, we estimate year-end income, confirm bracket targets, check IRMAA thresholds, and decide how much (if any) to convert. No autopilot—just disciplined, annual choices.

Remember that Roth conversions aren’t always optimal—higher-income years, ACA subsidies before Medicare, or tight cash for the conversion tax bill can tip the scales against converting in some years.

Find a Verified Fiduciary Advisor

Browse our directory of Orange Check verified advisors

Learn About the Fiduciary Standard

Understand what makes a true fiduciary advisor

Found this useful? Share it with your network.

Share on LinkedInAbout the Author

Related Articles

4 Summer Expenses People Forget to Budget For

Summer is a time for fun with friends & family, but it's also a time where it becomes easier to spend loosely. Here are 4 expenses most people forget to budget for this time of year

The One-Page Financial Plan Built for Freelancers and Content Creators

Most financial advice was built for people with one employer and one paycheck — not for freelancers and content creators juggling variable income, multiple revenue streams, and quarterly taxes. The one-page financial plan fixes that by breaking your entire financial picture down into five sections: cash flow and net worth, taxes, investments, risk analysis, and a 12-month action plan. It takes 1 to 2 hours the first time through and about 45 minutes every year after that. Come back to it once a

What to Do When a Parent Passes Away: A Guide for the First 90 Days

Losing a parent is difficult enough without having to navigate the financial and legal responsibilities that follow. I've worked with families after the loss of a parent, and one thing I've learned is that most people don't need more legal terminology during the first few weeks. They need someone to help them understand what should happen first, what can wait, and where costly mistakes are most often made. That's the purpose of this guide. This article isn't intended to replace advice from an estate attorney, CPA, or financial planner. Every estate is different. Instead, it provides a practical roadmap for navigating the first 90 days after losing a parent.